Capital adequacy

The Group’s capital adequacy is managed on the Bank level. It is aimed to ensure that the Bank's equity level is not lower than the one required by internal and external regulations. The regulations link the required capital level with the scale of operations and risks assumed by the Bank.

Considering the above, the Bank regularly:

- identifies risks material for its business;

- manages key risks;

- determines internal capital to be maintained should the risk materialize;

- calculates and reports capital adequacy measures;

- allocates internal capital to business areas;

- performs stress tests;

- compares its capital needs with the level of equity held;

- integrates the capital adequacy assessment with development of the Bank’s Strategy, financial and sales plans.

In 2016 the solvency ratio, Tier 1 and internal solvency ratio of the Bank were above the required regulatory minimum, which was 13.25% for CAR and -10.25% for Tier 1 (PFSA recommendation no. DRB/0735/2/1/2015).

In order to ensure high standards of capital management, compliant with best banking practices, once a year the Bank reviews the applicable policies and procedures.

Equity

For the purpose of equity calculation, the Bank applies methods arising from Regulation of the European Parliament and of the Council (EU) no. 575/2013 of 26 June 2013 on prudential requirements for credit institutions and investment firms and amending the Regulation (EU) no. 648/2012 (CRR). The Bank’s equity consists of Tier 1 (CET1) and Tier 2 capital.

In 2016, Tier 1 funds in the Bank included:

- equity instruments meeting the conditions specified in CRR;

- agio related to the instruments referred to above;

- retained earnings, to include current period gains or annual profit before a formal decision confirming the final financial performance for a given year following an approval of a competent body;

- accumulated other comprehensive income;

- reserve capital;

- general risk reserve;

- unrealized gains and losses measured at fair value (in amounts including transition regulations referred to in Articles 467 and 468 of the CRR);

- other Tier 1 items as determined in CRR;

and included adjustments due to:

- carrying amount of intangible assets;

- prudential filters and

- other items reducing Tier 1 funds as determined in CRR.

In June 2016 the Bank issued subordinated P1 bonds with the face value of PLN 50 million and maturity date of 8 June 2026. On 23 June 2016, the Bank obtained PFSA’s consent to classify the bonds as Tier 2 instruments (file no. DBK/DBK2/7100/5/4/2016/AN).

At the same time, in July 2016 the Bank prematurely redeemed subordinate BP0721 series bonds with the face value of PLN 47.34 million, which, pursuant to PFSA’s decision of 4 October 2011 (file no. DNB/IV/7100/2/5/IL/11) have been classified as Tier 2 funds of the Bank. On 23 June 2016 the Bank obtained PFSA’s consent to early redemption of the above bonds (file no. DBK/DBK2/7100/4/5/2016/AN).

As at 31 December 2016, Tier 2 funds in the Bank included cash obtained from a subordinate loan received in 2014 from Poczta Polska S.A. and two issues of subordinate bonds (carried out in 2012 and 2016, respectively).

Capital requirements (Pillar 1)

For the purpose of total capital requirement calculation, the Bank applies methods arising from CRR, in particular:

- the standard method of calculating the capital requirement due to credit risk,

- a simplified collateral recognition method where the counterparty’s risk weight is replaced with the collateral (its issuer’s) risk weight,

- the standard method of calculating the capital requirement due to operational risk,

- the standard method for the risk of credit valuation adjustment,

- the standard method of calculating the capital requirement due to currency risk,

- the maturity method of calculating the capital requirement due to general interest rate risk,

- the standard method of calculating the capital requirement due to special debt instrument price risk,

- the method of calculating the capital requirement due to large exposures.

Since the trading scale was immaterial, the capital requirement regarding market risks for the Bank was PLN 0.00. This means that in the analyzed period the Bank’s capital requirement was limited to credit risk, operational risk, currency risk and risk of credit valuation adjustment.

Internal capital (Pillar 2)

When identifying key risks that occur in the Bank’s operations, having included the scale and complexity of a given operation, additional risks are considered which, according to the management, are not fully covered by Pillar 1 risks. The identification is to allow optimum adjustment of the internal capital structure to actual capital needs, reflecting the actual risk exposure level.

For the additional risk purpose, the internal capital is calculated based on internal methods accepted by the Management Board, which include the scale and specifics of the Bank’s operations in a given risk context.

Additionally, when determining the internal capital, the Bank applies a conservative approach with regard to risk diversification among each risk type.

In 2016 the internal solvency ratio of the Group was above the required regulatory minimum.

Disclosures (Pillar 3)

Pursuant to the CRR and to the General Principles of Disclosing Information on Capital Adequacy in Bank Pocztowy S.A. accepted by the Supervisory Board of the Bank, in 2016 the Bank will publish information on its capital adequacy in a separate document.

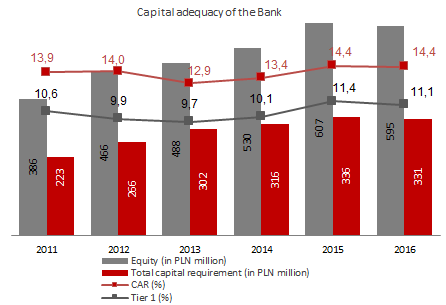

Capital adequacy of the Bank

As at 31 December 2014, 31 December 2015 and 31 December 2016 CAR and Tier 1 ratios were calculated in line with CRR. Pursuant to the above regulations, the Bank has been released from the obligation to determine its consolidated capital requirements. Separate data. In the remaining years CAR and Tier 1 values were calculated In accordance with Resolution no. 76/2010 of the Polish Financial Supervision Authority of 10 March 2010 regarding the scope and detailed principles of determining capital requirements due to various risk types (as amended). Separate data.

The following tables present a detailed calculation of base figures regarding equity, capital requirements and capital adequacy as at 31 December 2016 and 31 December 2015.

| Equity (in PLN’000) | ||

|---|---|---|

| 31.12.2016 | 31.12.2015 | |

| I Tier 1 capital | 460 126 | 480 417 |

| Equity instruments paid for | 110 133 | 110 133 |

| Agio | 55 356 | 55 691 |

| Retained earnings, including: | 2 724 | 25 086 |

| - profit (verified profit for the first half of the year) | 10 011 | 25 086 |

| - loss (a portion of not recognized current profit) | (7 287) | 0 |

| Accumulated other comprehensive income | (9 273) | 11 908 |

| Adjustments related to unrealized gains/losses on instruments in Tier 1 capital* |

(789) | (8 146) |

| Reserve capital | 252 862 | 225 577 |

| General risk reserve | 124 345 | 114 345 |

| Other intangible assets | (74 749) | (53 362) |

| Additional value adjustments arising from prudent measurement requirements | (483) | (815) |

| Tier 2 capital | 134 715 | 126 138 |

| Equity instruments and subordinated loans classified as Tier 2 capital | 134 715 | 93 000 |

| Adjustments related to instruments in Tier 2 capital in the transition period | 0 | 33 138 |

| Equity | 594 841 | 606 555 |

* The adjustment regards elimination of a portion of the positive valuation due to unrealized gains in the transition period.

| Capital requirements (in PLN ‘000) | ||

|---|---|---|

| 31.12.2016 | 31.12.2015 | |

| Capital requirements for credit, counterparty credit, dilution and settlement risk, including for exposures | 288 913 | 293 382 |

| with 0% risk weight | 0 | 0 |

| with 20% risk weight | 3 336 | 4 128 |

| with 35% risk weight | 41 643 | 43 364 |

| with 50% risk weight | 488 | 2 535 |

| with 75% risk weight | 170 588 | 176 316 |

| with 100% risk weight | 60 275 | 57 036 |

| with 150% risk weight | 4 189 | 5 454 |

| with 250% risk weight | 8 371 | 4 540 |

| other risk weights | 0 | 0 |

| due to payments to central counterparty fund in case of default | 23 | 9 |

| Capital requirement for operational risk | 42 319 | 41 270 |

| Capital requirement for currency risk | 0 | 1 201 |

| Capital requirement for credit valuation adjustment (CVA) | 12 | 51 |

| Total capital requirement | 331 244 | 335 904 |

| Solvency ratio | 14,4% | 14,4% |

| Tier 1 | 11,1% | 11,4% |

At the end of 2016, solvency ratio was 14.4%, while Tier 1 ratio was 11.1%, which denotes that the Bank’s operations ensured maintaining the capital measures above the required regulatory levels.

In 2016 the Bank was granted no financial support from public funds, in particular under the Act on granting the support for financial institutions by the State Treasury of 12 February 2009 (Journal of Laws of 2014 item 158).