Credit risk

Credit risk is the risk assumed by the Group under credit transactions and resulting in its inability to recover the amounts disbursed, loss of income or a financial loss. Its level is affected among others by quality of development and launch of a loan product, loan granting process and measures reducing the probability of losses. The Group’s credit risk includes both counterparty and settlement risk.

When developing its current credit risk management policy, the Group aims to maintain the risk appetite level, i.e. NPL, NPL cover ratio and the vintage curve. Other factors taken into account include maintaining an appropriate level of equity, compliance with the credit limits set by the Group, analyzing both strengths and weaknesses of the Group’s lending process and anticipating the opportunities and threats for its further growth. The Group’s acceptable credit risk policy also takes into account cyclicality of economic processes and changes in the credit portfolio itself.

The following principles have been adopted for the credit risk management process:

- analyzing credit risk of individual exposures, the entire portfolio and the capital requirement related to credit risk,

- applying internal and external limits arising from risk appetite in various areas of the credit portfolio and from the Banking Law and implemented recommendations of Polish Financial Supervision Authority, respectively;

- functions related to direct analysis of applications, risk assessment and credit related decision making are separated from those focused on client attraction (sales of banking products);

- creditworthiness is the main criterion underlying all credit transactions with clients;

- credit decisions are made in the Bank in accordance with procedures and competences determined in internal regulations on credit risk assessment and credit decision making;

- from conclusion to full settlement, each credit transaction is monitored in terms of utilization, timely repayment, legal security, equity and organizational relationships of the obligor and, in the case of institutional clients, also in terms of their current economic and financial position;

- developments in the real estate market as well as the legal and economic assumptions and framework for valuation of property provided as collateral for credit exposures are monitored on a periodic basis.

Credit risk management in the Group is based on written instructions and procedures defining the methods of identification, measurement, monitoring, limiting and reporting of credit risk. The regulations determine the scope of competences assigned to each unit of the Group in the credit risk management process.

In order to determine the credit risk level, the Group uses the following measures:

- probability of default (PD);

- recovery rate (RR);

- loss given default (LGD);

- loss identification period (LIP);

- share and structure of non-performing loans (NPL);

- coverage of non-performing loans with impairment losses (NPL coverage);

- scoring model efficiency measures (among others GINI, PSI ratio);

- cost of risk.

The Group carries out regular review of implementation of the adopted credit risk management policy. The following systems and ratios are subject to review and modification:

- internal regulations regarding client’s credit risk assessment and monitoring, as well as verification of the value of legal security, which are adjusted to changing market conditions, business specifics of each client type (group), loan purpose and determination of the minimum requirements regarding the obligatory forms of legal security;li>

- internal system of limiting credit activities and determining decision-making powers regarding loans;

- a system of identifying, assessing and reporting credit risk to Credit Committees, Management and Supervisory Board of the Bank;

- maximum adequacy levels of ratios used to assess credit risk and acceptable forms of own contribution for retail housing loans;

- scoring models and IT tools used in the credit risk management process.

The Group’s reporting system includes among others:

- reporting on credit risk level, to include vintage analyses, information regarding the use of limits, quality and efficiency of credit processes;

- reports on stress tests, limit review and back-test analyses for impairment losses;

- analyses of real property market and verification of the current value of security for credit exposures;

- review of implemented credit risk policy.

The Group prepares the following cyclical reports on its credit risk exposure:

- monthly report for the Management Board and Credit Committee of the Bank,

- quarterly report for the Supervisory and Management Board.

Portfolio quality

At the end of 2016 the share of exposures with recognized impairment in the total portfolio amounted to 8.9% and was 1.9 p.p. higher than at the end of 2015, on the one hand as a result of recognizing more impaired loans and on the other hand, due to reduced gross carrying amount of loans and advances. The increase in the value of impaired loan portfolio resulted from Bank’s focus on consumer loans market, which has given rise to a higher risk with assumed high profitability. Additionally, please note the risk profile regarding the cash and installment loan portfolio for years 2013-2016 being higher than initially assumed. Following the risk increase identification, in 2016 the Bank initiated measures aimed at its reduction.

| Portfolio quality – the share of impaired loans in the gross credit portfolio | ||||||

|---|---|---|---|---|---|---|

| 31.12.2012 | 31.12.2013 | 31.12.2014 | 31.12.2015 | 31.12.2016 | Change 2016/2015 | |

| Capital Group total | 4,7% | 5,4% | 6,1% | 7,0% | 8,9% | 1,9 p.p. |

| for individuals | 4,4% | 4,7% | 5,6% | 6,4% | 8,5% | 2,1 p.p. |

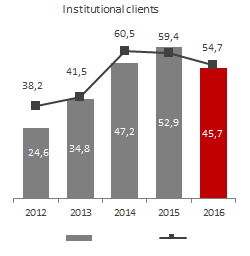

| for institutional clients | 9,5% | 12,3% | 13,0% | 15,4% | 15,7% | 0,3 p.p. |

| for local government bodies | 0,0% | 0,0% | 0,0% | 0,0% | 0,0% | 0,0 p.p. |

| Portfolio quality – impaired loans balance (PLN’000) | ||||||

|---|---|---|---|---|---|---|

| 31.12.2012 | 31.12.2013 | 31.12.2014 | 31.12.2015 | 31.12.2016 | Change 2016/2015 | |

| Capital Group total | 221 777 | 277 241 | 325 391 | 389 838 | 486 171 | 96 333 |

| for individuals | 157 472 | 193 465 | 247 265 | 300 766 | 402 603 | 101 837 |

| for institutional clients | 64 305 | 83 776 | 78 026 | 89 072 | 83 568 | (5 504) |

| for local government bodies | 0 | 0 | 100 | 0 | 0 | - |

Therefore, at the end of December 2016 the amount of loans with recognized impairment was PLN 96.3 million higher than at the end of 2015. Customer loans are the source of the entire increase, since in the institutional client segment the amount of impaired loans decreased.

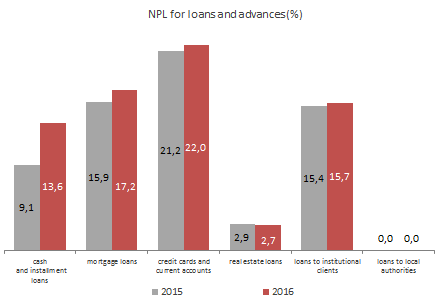

Below please find NPL per product group:

NPL for loans and advances (%)

Impairment losses

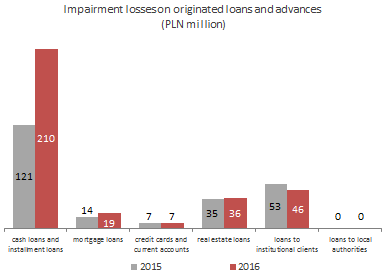

At the end of December 2016 the carrying amount of impairment losses for the Group’s loan portfolio was PLN 317.8 million and was 38.4% higher compared to the end of 2015, mostly as a result of increased impairment of cash and installment loans resulting from quality deterioration of that portfolio.

Impairment losses on originated loans and advances (PLN million)

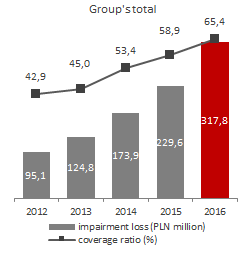

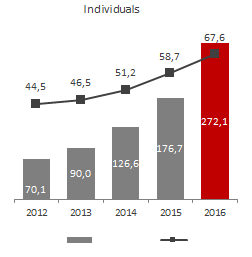

At the end of December 2016 the coverage ratio reached 65.4% and was 6.5 p.p. higher than at the end of December 2015. The ratio amounted to 67.6% for consumer loans and to 54.7% for institutional loans.

The calculation includes appropriation to IBNR.

Group's total

Individuals

Institutional customers