Activities in the consumer market

thousand new clients in

retail banking segemnt

At the end of 2015, services offered by Bank Pocztowy were used by 1,484.2 thousand consumers (individual and microenterprises), i.e. 51.9 thousand more than a year before.

The growing number of consumers confirms that the Bank's decision to create a simple and transparent offer built around trust and security has been appropriate. As a result, in 2015 the Bank acquired over 195 thousand new consumers.

After the ZawszeDarmowe (Always for free) account was introduced to the Bank’s offer in 2014 the number of consumers in the Bank’s portfolio started to grow dynamically in the following months. The largest increase was reported in the number of current account holders – by 82.2 thousand. At the same time, in line with the policy aimed at reducing costs of the deposit portfolio and adjusting the deposit balance to liquidity needs of the Bank, the number of deposit clients has decreased. The Bank reported a decrease in the number of clients holding term deposits by PLN 16.2 thousand. In 2015 the number of the Bank’s credit clients in the consumer segment grew by 7.9 thousand.

Development of the product offer for consumers

Bank Pocztowy has created a simple and comprehensible offer for consumers, including deposit, credit, investment, and insurance products. Following the strategy to simplify the offer, in the first half of 2015 the number of products and their variants has been limited.

The offer covers the following product groups:

- current account (Pocztowe Konto ZawszeDarmowe),

- saving account (Pocztowe Konto Oszczędnościowe),

- fixed-rate term deposits always offered in three term options: short-term MINI, mid-term MIDI, and long-term MAXI, i.e. as at 31 December 2015 it was respectively: 4, 6 and 36 months,

- floating-rate term deposits based on WIBID 3M – Market + 30M,

- 3-month deposit linked to acquisition of participation units in selected investment funds,

- consumer loans, cash loans, revolving overdrafts and credit cards,

- mortgage loans (including housing loans, mortgage loans and debt consolidation loans),

- insurance products,

- investment funds.

A current account for consumers is the key product used for acquiring consumers and the focal point in customer relationships.

On 1 April 2015 the Bank withdrew Pocztowe Konto Nestor targeted at senior consumers from its offer at the same time maintaining such accounts opened before that date. At the end of December 2015 the Bank managed 290 thousand active Nestor accounts, which constituted 32% of current accounts.

To drive acquisitions and transactional activities, in August 2015 the Bank launched a promotional action Opłaca się opłacać available to holders of ZawszeDarmowe accounts targeted at clients making payments to accounts. The promotion assumes that consumers will receive a PLN 100 bonus, i.e. get a portion of bills paid back from the Bank. The bonus is paid in the period of 5 months and is calculated as 10% of the amount of bills paid not to exceed PLN 20 per month.

Moreover, Bank Pocztowy has launched loyalty schemes and transactional activity programs to encourage its clients to actively use their personal accounts:

- Pakiet Pocztowy (postal package) program under which clients are refunded 10% of costs incurred for selected postal services offered by Poczta Polska (mainly packages and letters);

- Pocztowy Program Ubezpieczeniowy (postal insurance program) under which clients are refunded 10% of the insurance premium amount paid from their current accounts held with Bank Pocztowy under insurance agreements entered into with Pocztowe Towarzystwo Ubezpieczeń Wzajemnych and in co-insurance agreements with Sopockie Towarzystwo Ubezpieczeń Ergo Hestia S.A.,

- Program Aktywny Nestor (active nestor program) under which clients are refunded 5% of the amount paid for purchases made in any pharmacy in Poland and abroad provided that the payment has been made using a card linked to Pocztowe Konto Nestor (postal nestor account),

- Pay by link Envelo program for remote clients, under which they are refunded 10% of costs incurred to buy Envelo products through pay by link functionality from their accounts held with Bank Pocztowy.

Responding to clients’ needs, the Bank has extended its lending offer with:

- loan with the guaranteed lowest installment in the market sold under the brand name RataZawszeNajniższa,

- simple, short-term, low-value loan Pożyczka na Poczcie (from PLN 1 000 to PLN 3 000) offered since March 2015. The product launch was supported with an advertising campaign. In the second half of 2015 the repayment period was extended to 12 months and the acceptance of the statement of income was introduced for Pożyczka na Poczcie in the amount up to PLN 1 000.

A new simplified credit approval process was implemented in August 2015. Simplification of credit approval processes was one of the CODE initiatives. It will be easier, faster and more user-friendly for the client and for the Relationship Manager.

At the same time, the Bank communicated a message to clients focusing on the loan and installment amounts. It also introduced changes with respect to insurance constituting loan collateral, its scope, the sum insured and the method of calculating and collecting premiums. At the same time, the loan amount for which collateral is required has been changed. A new, semi-automatic processing path has been introduced. All these changes have been implemented along with a new cash loan credit approval process in the FerrytFlow application.

In April 2015 the term deposit offer was simplified by way of eliminating a number of product types and variants. In order to encourage clients to hold a personal account and to use remote banking services the Bank has increased interest rates on deposits made in the current account via the Internet or the Contact Center by 20 b.p.

The process of opening a current account was optimized in November 2015. The number of process steps has been limited, the workload for Relationship Managers has been reduced hence improving efficiency of customer service. Following the changes made an account may be opened within 15 minutes.

Since January 2015 the Bank, in cooperation with Ipopema TFI, has offered the possibility to purchase units in selected investment funds with a various investment strategy and risk profile. The funds’ offer constitutes and interesting alternative to the deposit offer for clients with a higher risk appetite. Investment products are available in the Bank’s sales network only.

The Bank also offers bancassurance products in cooperation with insurance companies, such as: Pocztowe Towarzystwo Ubezpieczeń Wzajemnych, Aviva Towarzystwo Ubezpieczeń na Życie S.A., Aviva Towarzystwo Ubezpieczeń Ogólnych S.A. and Pocztowe Towarzystwo Ubezpieczeń na Życie.

At the beginning of 2015 numerous regulatory changes were implemented, hence the Bank had to adjust its insurance operations to the requirements determined by the Polish Financial Supervision Authority in Recommendation U. Due to regulatory changes the Bank had to carry out a business assessment of insurance products with particularly low insurance premiums. Consequently, it was necessary to eliminate credit card and debit card insurance and accident insurance to overdrafts from the Bank's offer.

In cooperation with Pocztowe Towarzystwo Ubezpieczeń Wzajemnych and Pocztowe Towarzystwo Ubezpieczeń na Życie the Bank introduced correlated insurance products to its offer: a life insurance package, health and non-life insurance with various sums insured and premiums determined by clients based on their needs. A life insurance and income protection insurance have been included in the offer related to the cash loan.

An important process change was also introduced in 2015, which included the change in the method of calculating and collecting insurance premiums from clients. The insurance premium is no longer calculated and charged on a one-off basis, but it is payable monthly. The change proved very important for clients, as it enabled prorating the cost of insurance over a period of time.

The insurance coverage for borrowers using cash loans includes unemployment insurance, accident insurance and life insurance. The offer for mortgage loan borrowers has remained unchanged. The Bank offers real estate insurance and life and unemployment insurance packages.

Credit operations

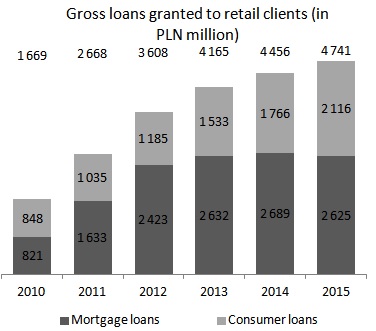

At the end of 2015 gross credit receivables of Bank Pocztowy from consumers totaled PLN 4 741.3 million versus PLN 4 454.7 million in December 2014 (a 6.4% increase). The Bank’s share in credit receivables from consumers of the banking sector amounted to 0.9%.

| Gross loans granted to clients of Bank Pocztowy S.A. in the retail segment (PLN’000) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 31.12.2015 | structure (31.12.2015) | 31.12.2014 | structure (31.12.2014) |

|

|||||||

| Gross loans and advances, including: | 4 741 255 | 100,0% | 4 454 674 | 100,0% | 286 581 | 6,4 % | |||||

| Mortgage loans | 2 625 126 | 55,4% | 2 689 295 | 60,4% | (64 169) | (2,4)% | |||||

| Consumer loans | 2 116 129 | 44,6% | 1 765 379 | 39,6% | 350 749 | 19,9 % | |||||

Source: management information of the Bank. The data present the principal amount only. Default interest, due and undue interest, commissions, other prepaid expenses and revenue, other restricted revenue and interest and other receivables were not included. Consumer loans includes cash and installment loans, overdrafts and credit card debt and the principal amount balance of loans granted to microenterprises which amounted to PLN 39 308 thousand as at 31 December 2015, as compared to PLN 43 933 thousand as at 31 December 2014. The item does not include the balance of mortgaged loans for consumption purposes, which were presented in mortgage loans.

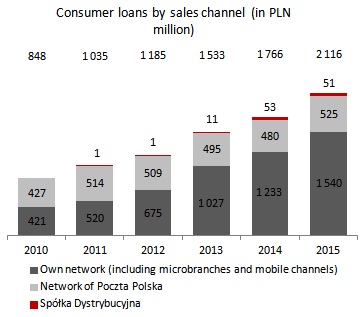

In 2015 the Bank dynamically acquired new consumer loans. At the end of December 2015 receivables due to such products reached PLN 2,116.1 million, i.e. by 19.9% more than a year before. In 2015 the Bank sold consumer loans with the value of more than PLN 1 billion.

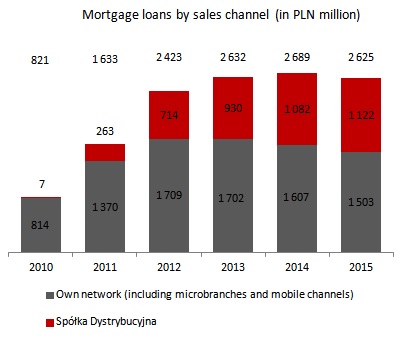

Mortgage loans remain a large portion of the portfolio. As at 31 December 2015, the Bank’s receivables due to mortgage loans reached PLN 2,625.1 million and were by 2.4% lower than in December 2014. In 2015 the Bank, offering local currency loans only, extended PLN 106.2 million of mortgage loans, i.e. by 48.1% less than in 2014, when the sales reached PLN 204.6 million. The decrease resulted from the strategy followed. Due to limited capital, the Bank focuses on the sale of products with the highest profitability considering their effect on the capital, which implies promoting the sale of consumer loans.

Spółka Dystrybucyjna is at present the only distribution channel for mortgage loans. The key distribution channels are own sales network and the offices of Poczta Polska.

Gross loans granted to retail clients (in PLN million)

Consumer loans by sales channel (in PLN million)

Mortgage loans by sales channel (in PLN million)

In the years 2013-2015 cross-selling activities, i.e. the sale of products to the existing client portfolio under the approved limits, grew dynamically. The strategy was aimed at increasing the volume of loans granted to clients, and consequently growing their profitability. This was achieved through:

- an increase in the number of communications sent to clients from 70 in 2013 to nearly 200 in 2015; hence the total number of client communications grew to ca. 600 thousand p.a.,

- cyclical retention actions addressed to clients with maturing loans,

- cyclical additional sales of loans based on a simplified process developed in line with Recommendation T covering 1/3 of the client base,

- extending the sales channels in the cross-sell actions to include own outlets and the network of Poczta Polska,

- implementing Operational CRM, which enables contact distribution to the Bank's sales network and recording results,

- initiating development of a multi-channel process, where the Call Center calls clients from the database and reports sales leads for further processing by the sales network.

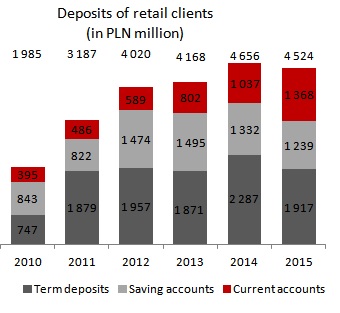

Deposits

In 2015 the Bank adjusted the speed of developing its deposit base to credit needs, including optimization of the funding costs. At the end of December 2015 consumers deposited in the Bank the total of PLN 4,523.5 million versus PLN 4,656.2 million at the end of December 2014 (a decrease by PLN 132.7 million). Consequently, the Bank's share in consumer's deposits market8 reached 0.7%.

| Deposits of Bank Pocztowy S.A. - retail segment (in PLN ‘000) | |||||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|

| 31.12.2015 | structure (31.12.2015) | 31.12.2014 | structure (31.12.2014) |

|

|||||||

| Client deposits, including: | 4 523 510 | 100,0% | 4 656 169 | 100,0% | (132 659) | (2,8)% | |||||

| Current accounts | 1 367 747 | 30,2% | 1 036 810 | 22,3% | 330 936 | 31,9% | |||||

| Savings accounts | 1 238 990 | 27,4% | 1 332 618 | 28,6% | (93 628) | (7,0)% | |||||

| Term deposits | 1 916 773 | 42,4% | 2 286 741 | 49,1% | (369 968) | (16,2)% | |||||

Source: management information of the Bank. The data include only the principal balance of deposits of individuals and microenterprises, without accrued interest. As at 31 December 2015 the balance of deposits of microenterprises amounted to PLN 116 649 thousand, while as at 31 December 2014 it was PLN 91 100 thousand. Interest accrued were not included.

In 2015, funds deposited on current accounts of consumers increased to reach PLN 1 367.7 million at the end of December 2015 (31.9% more than in December 2014).

At the end of 2015 Bank Pocztowy managed more than 1 million active current accounts of consumers:

- 908.8 thousand current accounts, i.e. by 87.7 thousand more than at the end of 2014. An introduction of ZawszeDarmowe account to the Bank’s offer in September 2014, which is expected to be maintained free of charge for an indefinite period, enabled mass client acquisition. In 2015 the Bank concluded over 225 thousand new current account agreements. Nestor accounts, which were no longer sold since 2015 amounted to 290 thousand (32% of the total current account portfolio).

- 176.6 thousand of Pocztowe Konto Firmowe accounts for microenterprises, i.e. by 0.4 thousand more than at the end of 2014.

Deposits of retail clients (in PLN million)

In December 2015 consumers deposited PLN 1 239.0 million on saving accounts in the Bank, i.e. by 93.6 million less than at the end of 2014. The decrease resulted from the deposit structure change aimed at reducing the costs of the deposit portfolio.

Due to decreasing interest rates the lowest demand was reported for term deposits. At the end of December 2015 funds placed in term deposits amounted to PLN 1 916.8 million and were PLN 370.0 million lower than at the end of 2014.

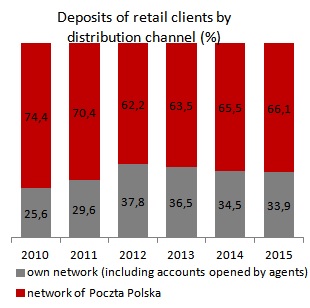

In December 2015, 66.1% of funds deposited with Bank Pocztowy came from consumers and were collected through the Poczta Polska network:

- current accounts – 79.9% (versus 80.5% in December 2014),

- saving accounts – 63.0% (versus 61.3% in December 2014),

- term deposits – 58.3% (versus 61.3% in December 2014).

Deposits of retail clients by distribution channel (%)

Deposits of retail clients by type and distribution channel (in PLN million)

Investment products

In 2015 the Bank sold investment fund units with the value of PLN 206 million, which implies a high demand for such products among the Bank’s clients.

Works are carried out to introduce investment fund units to the Bank' s offer to be sold as white label products - Pocztowy Specjalistyczny Fundusz Inwestycyjny Otwarty. A necessary request was filed with the Polish Financial Supervision Authority by Ipopema TFI. The products of Pocztowy SFIO are expected to be offered starting from Q2,2016.

In Q1,2015 the Bank withdrew a structured product Światowi Giganci and a unit-linked insurance product Złote Jutro from its offer intending to simplify its investment offer and to focus on the sale of investment fund units.

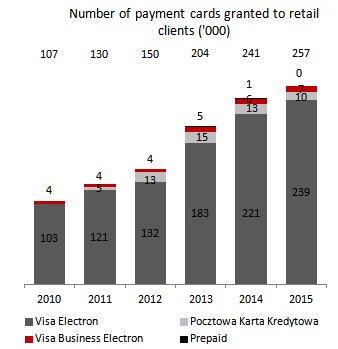

Bank cards

Bank Pocztowy offers the following types of bank cards to consumers:

- MasterCard and Visa Electron debit cards issued to personal accounts,

- MasterCard and Visa Classic credit cards,

- Visa Business cards issued to Pocztowe Konto Firmowe accounts.

At the end of 2015 the payment card portfolio for consumers amounted to PLN 257 thousand, out of which 93% were debit cards.

Major changes in the payment card offer of the Bank:

- at the beginning of 2015 the possibility to enable and to disable the contactless payment functionality has been implemented,

- in order to enhance security on 1 February 2015 the Bank introduced the possibility for consumers to establish an individual limit for online transactions,

- Debit cards to Pocztowe Konto Oszczędnościowe and pre-paid cards were withdrawn from the offer on 1 April 2015,

- Following the implementation of Recommendation U on 1 April 2015 additional insurance coverage Ochrona karty (card protection) and additional optional insurance coverage for repayment of credit card debt have been withdrawn from the offer.

Number of payment cards granted to retail clients ('000)