General information about the Capital Group

Bank Pocztowy (Bank) is a consumer bank providing safe and simple financial services through the network of Poczta Polska, its own offices operating countrywide and through mobile channels. Its business model is based on strategic partnership with Poczta Polska, which ensures exclusive access to its distribution network and a wide consumer portfolio in provincial Poland.

The mission of the Bank is defined as “simple, safe and well-priced banking”.

For consumers it implies:

- focus on the simplest products, processes and communication;

- good price guaranteed to a wide group of consumers;

- modern financial services based on integration within the Poczta Polska Capital Group.

Bank Pocztowy focuses on consumer banking and provides a supplementary offer for microenterprises.

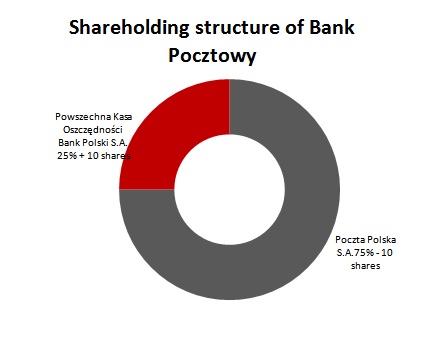

Poczta Polska S.A. is the key shareholder and business partner of Bank Pocztowy holding 75%, i.e. 10 shares in its share capital. Powszechna Kasa Oszczędności Bank Polski S.A. also holds shares in the bank (25% +10 shares).

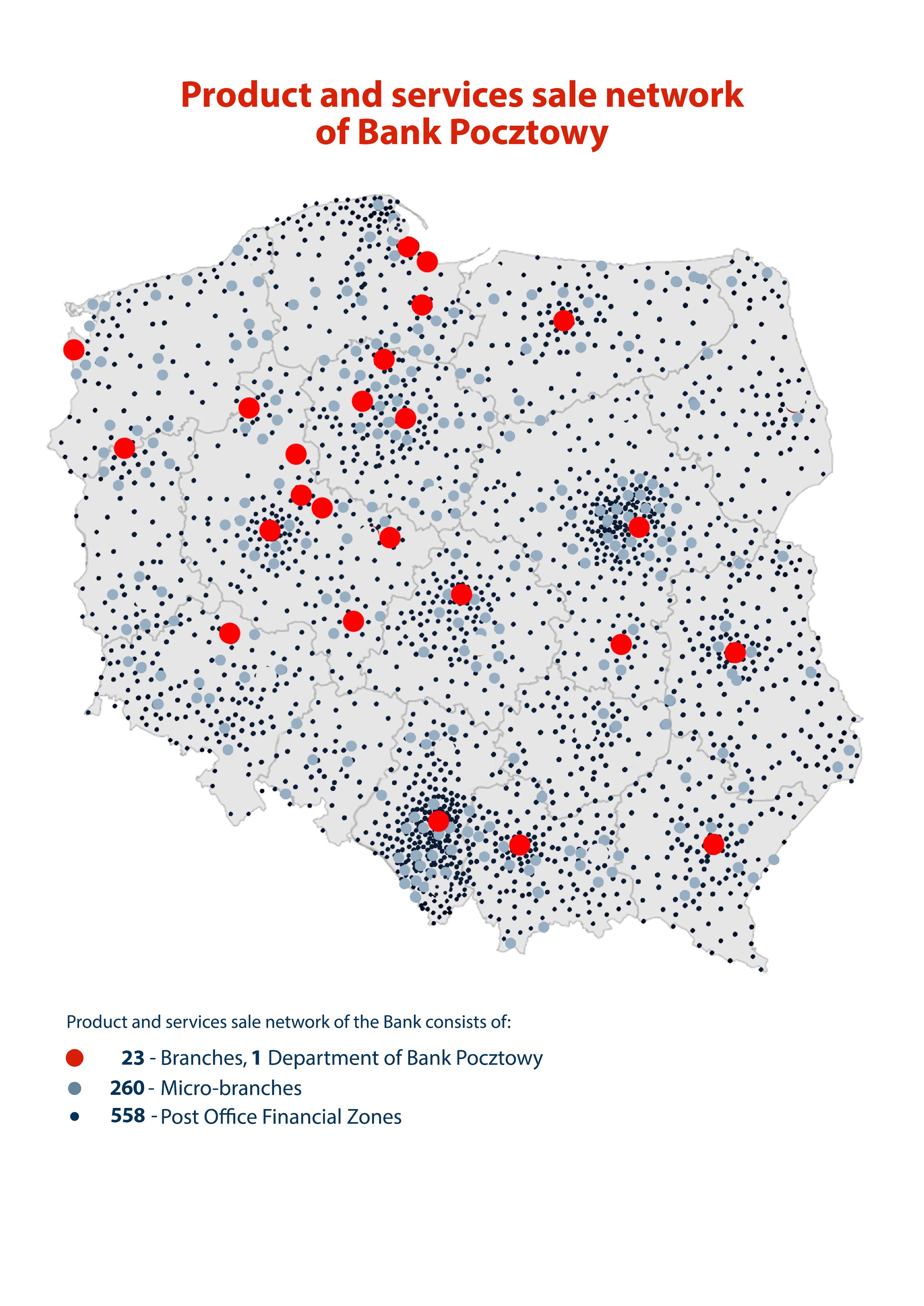

Thanks to the strategic alliance with Poczta Polska, the Bank’s services and products are available in ca. 7.4 thousand outlets and offices (post offices, branches and agencies) countrywide. Apart from Poczta Polska, Bank Pocztowy offers its services and products through 284 own offices, electronic distribution channels (online and telephone banking) and a network of mobile agents of its subsidiary – Spółka Dystrybucyjna Banku Pocztowego Sp. z o.o. Additionally, the Bank’s products are distributed by ca. 23 thousand postmen and other agents. The wide distribution network constitutes a unique competitive advantage of the Bank.

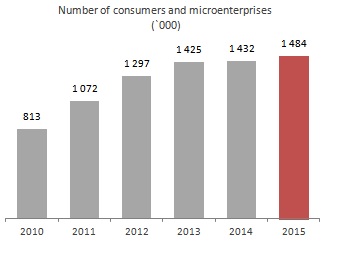

At the end of 2015 the Bank provided services to 1,484.2 thousand consumers and microenterprises. In 2015 it acquired 195.3 thousand new clients in this group. The Bank served over 15.2 thousand of entities in the institutional segment. Consequently, at the end of 2015 the Bank had about 1.5 million clients in consumer and institutional segments.

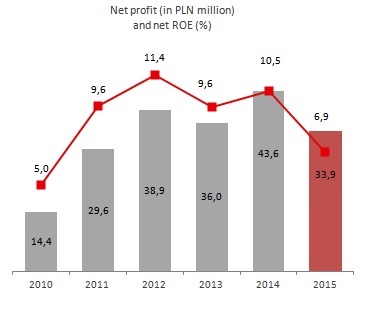

In 2015 the Group generated the net profit of PLN 33.9 million and ROE of 6.9%.

Number of consumers and microenterprises ( '000)

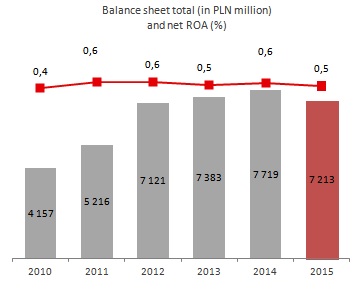

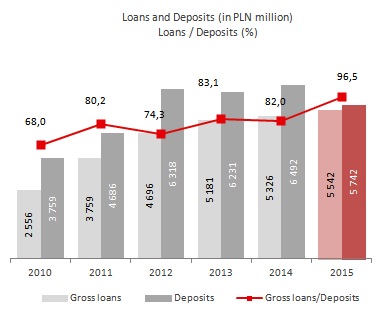

As at 31 December 2015, the balance sheet total of the Group amounted to PLN 7,213.0 million and represented 0.5% of the total assets of the Polish banking sector[1]. The total gross loans and advances granted to clients amounted to PLN 5,542.5 million with 85% of consumer loans. Liabilities to the Bank’s clients amounted to PLN 5 742.4 million, including over 77.4% of funds obtained from the consumer sector. With its 3%[2] share, the Bank has gained a relatively good position in the current accounts market thanks to dynamic growth reported in the last few years and the increase in the number of consumers.

Net profit (in PLN million) and net ROE (%)

At the end of 2015 employment in the Group reached 1,618 FTEs.

Balance sheet total (in PLN million) and net ROA (&)

Bank Pocztowy’s bonds have been listed with Catalyst. The Bank’s position as a responsible issuer caring for high standards of communication with the capital market has been confirmed with the award in The Best Annual Report contest for 2014 in the category of Banks and Financial Institutions which was granted to the Bank for the second time in a row. The Bank got the second place and was recognized for the application of the IFRS/IAS in the financial statements.

Subsidiaries of the Bank Pocztowy Group play an important role in implementing the strategy of the Capital Group. They include:

- Spółka Dystrybucyjna Banku Pocztowego Sp. z o.o., whose key objective is to support distribution channels of Bank Pocztowy and access prospect clients from remote locations.

- Centrum Operacyjne Sp. z o.o. (Centrum Operacyjne) providing professional services in process administration for products and services for entities in the financial sector.

Loans and Deposits (in PLN million) Loans/Deposits (%)

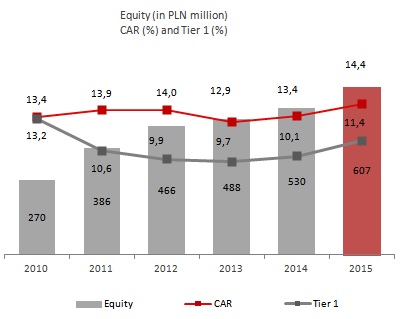

Equity (in PLN million) CAR (%) and Tier 1 (%)

1 Source: Financial Supervision Authority, monthly data for the banking sector file – December 2015.

2 Source: PRNews.pl Rynek kont osobistych – Q3,2015, 01.12.2015.

Bank history

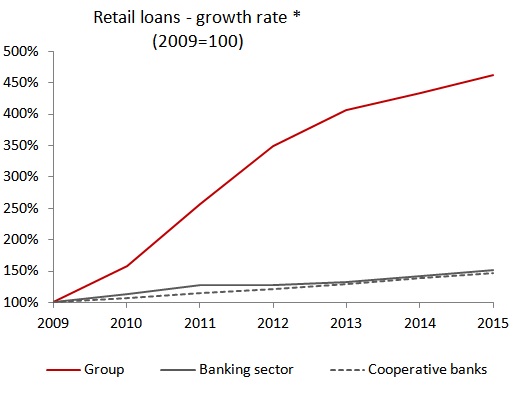

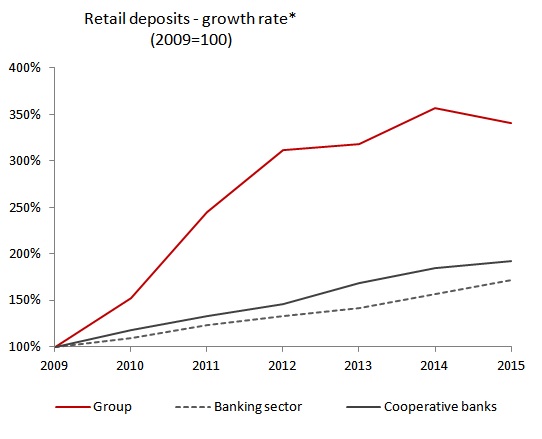

The Group benchmarked against the banking sector and cooperative banks

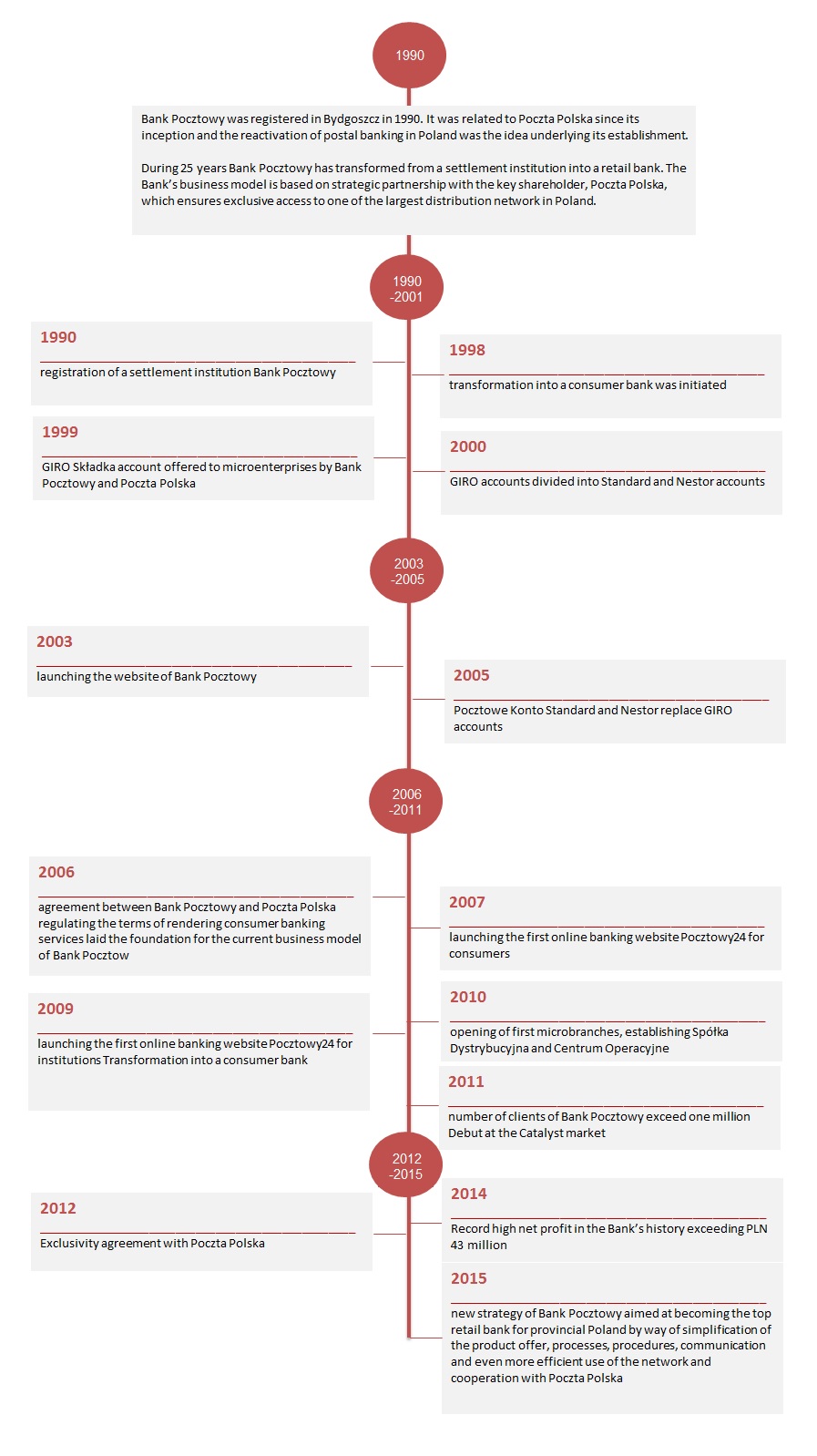

Bank Pocztowy started operations in 1990. Reactivation of postal banking in Poland was the idea underlying its establishment. To this aim and in order to develop Bank Pocztowy S.A. the GIRO non-cash settlement system was launched to enable fast and easy processing of bulk payments, reduce costs of issuing and circulating cash in the economy and to provide bank services to clients, in particular consumers, through a wide distribution network of Poczta Polska. Therefore, initially the Bank was a typical settlement institution with performance highly related to the volume of settlements with Poczta Polska.

In 1998, transformation into a consumer bank was initiated. The Bank started to reach an increasingly large group of clients through a sales network of Poczta Polska and own branches and sales points. At the same time, it started to launch new products.

In 1999 all post offices provided comprehensive services related to GIRO personal accounts and, additionally, Visa Electron cards to the accounts were offered. In 2003, the Bank launched an online information system. Two years later, in 2005, GIRO personal accounts were renamed to Pocztowe Konto Nestor for elderly people and Pocztowe Konto Standard.

Agreement concluded by Bank Pocztowy and Poczta Polska in 2006 regulating the terms of cooperation between the institutions in consumer banking services was a breakthrough event for the Bank's consumer business. Under the agreement over 2 thousand Postal Financial Points were opened in post offices by the end of 2009 to streamline service provision to the Bank’s customers by post office staff. Following the gradual changes and development of the sales network, in February 2010 the number of clients exceeded 500 thousand, in October 2011 it was 1 million, and now it its approaching 1.5 million. Along with the growth in the number of clients, the Bank has consistently improved its profitability, as indicated by a regular increase of its financial profit and ROE.

In 2010 the Bank’s subsidiaries: Spółka Dystrybucyjna Banku Pocztowego Sp. z o.o. and Centrum Operacyjne Sp. z o.o. were established and commenced business activities. As a result ,the Bank Pocztowy Capital Group was set up.

| Key data of the Bank Pocztowy S.A. Capital Group for 2010-2015 | |||||||

|---|---|---|---|---|---|---|---|

| 2010 | 2011 | 2012 | 2013 | 2014 | 2015 | Change 2015/2014 | |

| Key financial data | |||||||

| Group’s income 1/ (PLN’000) | 221 165 | 258 473 | 290 255 | 294 320 | 332 340 | 327 528 | (1,4)% |

| Administrative expenses (PLN ‘000) | (195 204) | (209 837) | (218 356) | (212 738) | (218 622) | (217 030) | (0,7)% |

| Impairment losses (PLN’000) | (9 673) | (12 877) | (25 099) | (42 398) | (61 013) | (66 145) | 8,4 % |

| Gross profit (PLN ‘000) | 17 529 | 37 531 | 48 665 | 43 260 | 55 145 | 42 879 | (22,2)% |

| Net profit (PLN ‘000) | 14 412 | 29 555 | 38 949 | 36 027 | 43 639 | 33 931 | (22,2)% |

| Balance sheet | |||||||

| Balance sheet total (PLN ‘000) | 4 156 609 | 5 215 801 | 7 120 653 | 7 382 745 | 7 719 027 | 7 213 030 | (6,6)% |

| Loans and advances granted to clients 2/(PLN’000) | 2 488 835 | 3 679 382 | 4 599 545 | 5 055 712 | 5 151 777 | 5 312 882 | 3,1 % |

| Liabilities to customers (PLN’000) | 3 759 124 | 4 685 735 | 6 317 949 | 6 230 578 | 6 492 023 | 5 742 377 | (11,5)% |

| Equity (PLN ‘000) | 294 968 | 321 395 | 361 470 | 391 765 | 439 632 | 542 485 | 23,4 % |

| Key ratios: | |||||||

| Net ROA (%) | 0,4 | 0,6 | 0,6 | 0,5 | 0,6 | 0,5 | (0,1) p.p. |

| Net ROE (%) | 5,0 | 9,6 | 11,4 | 9,6 | 10,5 | 6,9 | (3,6) p.p. |

| Expenses with amortization (depreciation) / income (C/I)3 (%) | 87,8 | 80,6 | 74,7 | 71,3 | 65,3 | 66,6 | 1,3 p.p. |

| Solvency ratio 4 /(%) | 13,4 | 13,9 | 14,0 | 12,9 | 13,4 | 14,4 | 1,0 p.p. |

| Tier 1 4/ (%) | 13,2 | 10,6 | 9,9 | 9,7 | 10,1 | 11,4 | 1,3 p.p. |

| NPL 5/ (%) | 7,2 | 5,0 | 4,7 | 5,4 | 6,1 | 7,0 | 0,9 p.p. |

| Net interest margin to total assets / (%) | 3,6 | 4,1 | 3,8 | 3,6 | 3,8 | 3,6 | (0,2) p.p. |

| Business figures: | |||||||

| Headcount (FTEs) | 1 323 | 1 496 | 1 571 | 1 700 | 1 633 | 1 618 | (0,9)% |

| Number of offices | 74 | 161 | 227 | 295 | 293 | 284 | (3,1)% |

| Number of customers and microenterprises (‘000) | 813 | 1 072 | 1 297 | 1 425 | 1 432 | 1 484 | 3,6 % |

1.Net interest income, net fee and commission income, gain/loss on financial instruments measured at fair value through profit or loss and realized gain/loss on transactions on securities available for sale.

2.Net loans and advances.

3.Income increased by gain/loss on other revenue and operating expenses.

4.NPL (non-performing loans) – the share of impaired loans and advances in the entire credit portfolio.

5. Interest margin – a relation of net interest income to average assets (calculated as average daily balance of assets)

The Group benchmarked against the banking sector and cooperative banks

In 2015 the Group focused on the offer targeted at consumers, in particular on consumer loans. Following the policy adopted, in 2015 the Group further increased the share of exposures granted to individuals in the total credit portfolio. At the end of 2015 such exposures accounted for 85.0%, i.e. were by 1.9 p.p. higher than the previous year.

* Market data – household analysis.

The growth in loans and advances granted by the Group to consumers in the years 2009-2015 was much higher than in the entire banking sector and in the group of cooperative banks. The average annual growth rate of the discussed loans in the analyzed period amounted to 29.1% vs. 7.1% growth in the banking sector and 6.5% growth in the group of cooperative banks.

Similarly, the growth in deposits of consumers in the years 2009-2015 was considerably higher than in the entire banking sector and in the group of cooperative banks. The average annual growth in consumer deposits acquired by the Group in the years 2009-2015 amounted to 22.7%. The average annual growth in liabilities to consumers in the entire banking sector in the same period was 9.4% and 11.5% in the group of cooperative banks. In the recent years, stable deposits of consumers accounted for two thirds of the total value of deposits.

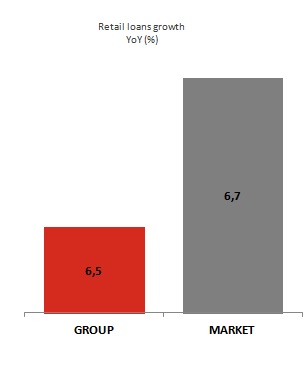

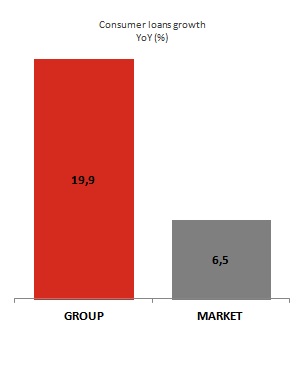

At the end of December 2015 receivables arising from loans granted to individuals amounted to PLN 4 711.4 million and grew by 6.5% p.a., as compared to the 6.7% growth in the banking sector. In 2015, the Group reported a three times higher growth of consumer loans than that of the banking sector.

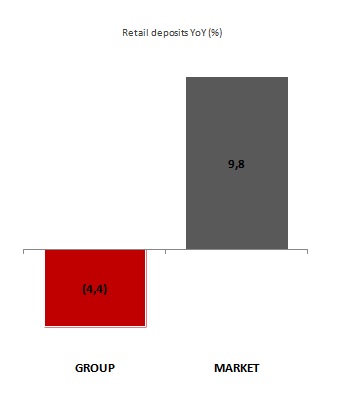

Due to low market rates, clients were less willing to deposit funds in 2015. At the end of December 2015, total liabilities of the Group to individuals dropped by 4.4% and amounted to PLN 4 444.9 million.

Retial loans growth YoY (%)

Consumer loans growth YoY (%)

Retail deposits YoY (%)

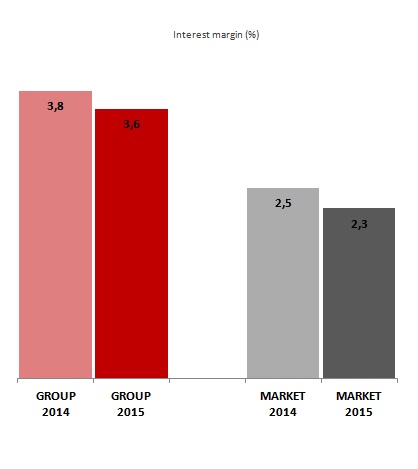

Record low interest rates resulted in a 0.2 p.p. decrease in interest margin in the banking sector and in the Group. Significantly, the Group’s margin was considerably higher than in the entire banking sector.

A series of one-off events resulting in considerable financial charges affected the profit of the Group and of the entire banking sector: increasing the additional payment to the Bank Guarantee Fund related to the bankruptcy of Spółdzielczy Bank Rzemiosła i Rolnictwa seated in Wołomin („SK Bank”) up to PLN 2 billion and the cost of payments made to the Borrowers Support Fund established under the Act on supporting borrowers in a difficult financial situation who have been granted a mortgage loan of 9 October 2015 of PLN 600 million.

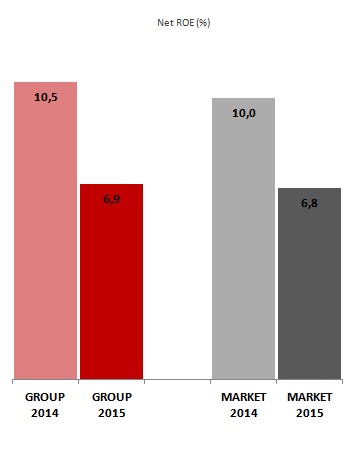

Consequently, in 2015 the Group’s net ROE amounted to 6.9% and was by 0.1 p.p. higher than the net ROE of the banking sector.

Interest margin (%)

Net ROE (%)

Interest margin, ROE for the banking sector – the denominator specifies the asset level with interest margin and capital level for ROE at the end of 2015 and the end of 2014.